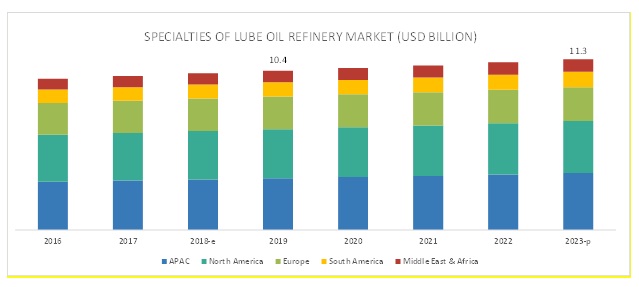

The specialties of lube oil refinery market has been studied for APAC, North America, Europe, South America, and the Middle East & Africa. The APAC specialties of lube oil refinery market is projected to register the highest CAGR, in terms of value, during the forecast period. The global specialties of lube oil refinery market has witnessed a sluggish growth, owing to the slow growth in North America and Europe. This created huge opportunities for the consumption of specialties of lube oil refinery in APAC. Change in lifestyle and purchasing power parity of the consumers in this region is also driving the use of specialties of lube oil refinery in the cosmetics, pharmaceutical, and packaging industries.

The specialties of lube oil refinery market is expected to grow from USD 10.4 billion in 2018 to USD 11.3 billion by 2023, at a CAGR of 1.8%. The growth of the specialties of lube oil refinery market is attributed to the growing packaging, pharmaceutical, and cosmetics industries.

To know about the assumptions considered for the study download the pdf brochure

Companies such as Exxon Mobil Corporation (US), Sinopec Corporation (China), Royal Dutch Shell Plc (Netherlands), PetroChina Company Limited (China), Repsol SA (Spain), Eni S.p.A. (Italy), LUKOIL (Russia), and Sasol Ltd. (South Africa) are the leading players in the specialties of lube oil refinery market, globally. Diversified product portfolio, high depth in application reach, and technical assistance to customers are factors responsible for strengthening the position of these companies in the specialties of lube oil refinery market. They have also been adopting various organic and inorganic growth strategies, such as new product development, merger & acquisition, and expansion, to enhance their current position in the specialties of lube oil refinery market.

Sinopec Corporation (China) is the other major player in the specialties of lube oil refinery market. The company adopted the inorganic growth strategies to establish its foothold, globally. For example, Gaoqiao Petrochemical Co Ltd. (China), a wholly owned subsidiary of Sinopec Corporation, purchased the 50% stake of BP Group (UK) in the Shanghai SECCO Petrochemical Company Limited (SECCO) and formed a 50-50 joint venture with Shanghai Secco Petrochemical. In January 2016, Sinopec Corporation entered into a joint venture with Saudi Aramco (Saudi Arabia) for strategic co-operation to set up a refinery Yanbu Aramco Sinopec Refining Company at Riyadh, Saudi Arabia. With this joint venture, the company plans to build strong business relationships with customers in the Middle East and improve its position in the specialties of lube oil refinery market.

Scope of the Report:

| Report Metric | Details |

| Market size available for years | 2016-2023 |

| Base year considered | 2017 |

| Forecast period | 2018–2023 |

| Forecast units | Value (USD), Volume (Kiloton) |

| Segments covered | Type and Region |

| Regions covered | North America, APAC, Europe, South America, and Middle East & Africa |

| Companies covered | Exxon Mobil Corporation (US), Sinopec Corporation (China), Royal Dutch Shell Plc (Netherlands), Eni S.p.A. (Italy), Sasol Ltd. (South Africa) Total 25 major players covered |

To speak to our analyst for a discussion on the above findings, click Speak to Analyst