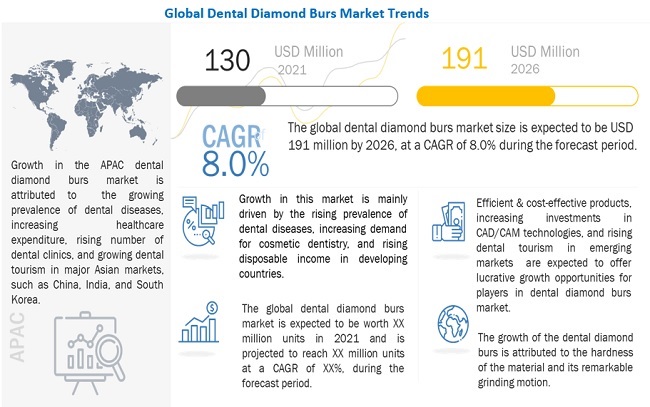

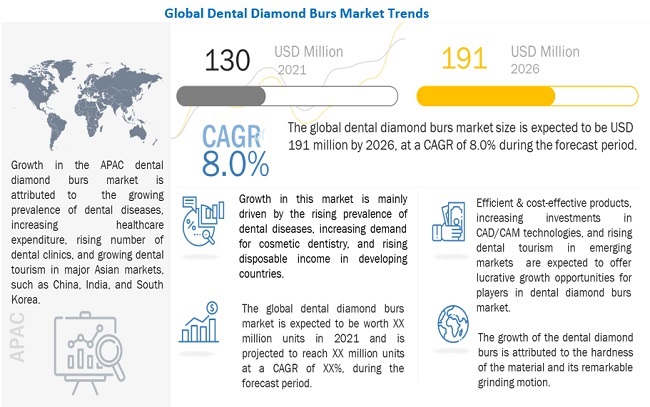

The global dental diamond burs market size is estimated at USD 130 million in 2021 and is projected to reach USD 191 million by 2026, at a CAGR of 8.0%, between 2021 and 2026. Dental diamond burs are restorative instruments. Dentists utilize diamond burs all around the world, most commonly with high-speed handpieces. The most common application of dental diamond burs is to grind away hard tooth tissue, generally enamel and bones. A diamond bur’s grinding action produces a rough surface. They are made by bonding small diamond particles to a substrate. They find their best use when a cut demands high accuracy is required.

The North America region is projected to be the largest market, in terms of value. APAC is expected to grow at the highest CAGR during the forecast period. Growth in North America is backed by The increasing cases of dental diseases, growing demand for tooth repair procedures, growth in the geriatric population, increasing number of dental practitioners, and rising number of dental clinics and dental laboratories.

To know about the assumptions considered for the study download the pdf brochure

Moreover, the growth in this market is driven by a number of factors, such as the rising geriatric population, growing dental tourism in major Asian markets, such as India, increasing focus of prominent players on emerging Asian countries, increasing healthcare expenditure (coupled with the rising disposable income), growing awareness on oral healthcare, and increasing willingness of people to spend more on dental care to maintain dental aesthetics. Other factors, such as the increasing number of dental professionals, rising cases of dental diseases, and growing number of tooth repair procedures, are expected to support the growth of this regional market during the forecast period.

The key players in the dental diamond burs market are Dentsply Sirona Inc. (US), Henry Schein, Inc. (US), SHOFU Inc. (Japan), MANI, INC. (Germany), Bresseler USA (US), and others. The dental diamond burs market report analyzes the key growth strategies adopted by the leading market players, between 2016 and 2021, which include expansions, mergers & acquisition, new product developments/launch, and collaborations.

Henry Schein, Inc. is a healthcare solutions company. It is one of the world’s leading providers of healthcare products and services, particularly to dental and medical practitioners in their offices, as well as alternate care settings. The company conducts its business through three reportable segments, health care distribution, technology and value-added services, and Corporate TSA Revenues. The company manufactures dental specialty products in the areas of implants, orthodontics, and endodontics. It has its operations in 31 countries across the globe. It has 28 strategically-located distribution centers around the world. It is a fortune 500 company.

MANI, INC. engages itself in the development, manufacture, and sale of medical instruments specializing in surgical and dental products. The company started manufacturing surgical needles in 1956 and since has contributed as a medical device manufacturer supplying surgical and dental instruments. In order to actualize high-quality and low-cost production technologies, the firm has production facilities in Vietnam, Myanmar, and Laos. The company focuses largely on the R&D. It has three reportable segments, namely, surgical products (products related to the surgical and ophthalmic fields), eyeless products (Suture Needles: Eyeless・ Eyed) and Dental Products. The dental product segment includes R&D, manufacture, and distribution activities for the dental medical devices, such as dental instruments, root canal treatment instruments, endodontic rotary cutting instruments, and endodontic accessories. The company was listed on second section of Tokyo Stock Exchange in 2011.

Request for Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=86086144