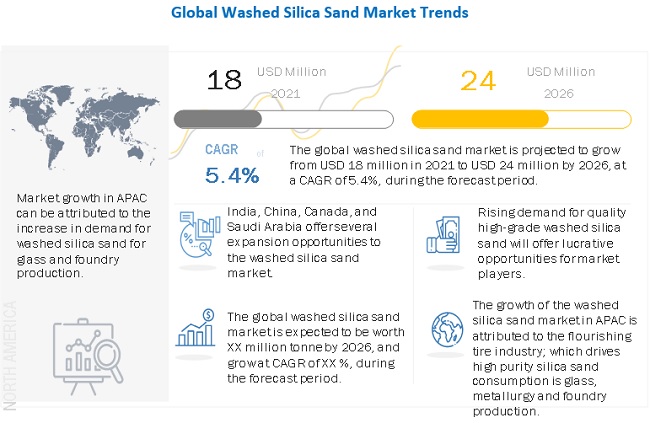

The global washed silica sand market size is projected to grow from USD 18 million in 2021 to USD 24 million by 2026, at a Compound Annual Growth Rate (CAGR) of 5.4% during the forecast year. Washed silica sand refers to silica sand that undergoes a washing and rinsing process after mining. Salt, clay, and other powders and dust are washed out of the overall mixture. It often undergoes additional separating and classification into grain sizes or grit sizing. Washed silica sand comes in coarse, medium, fine, and ultra-fine granule sizes. Washed silica sand is used for various applications, such as glass, foundry, ceramic & refractories, filtration, abrasives, metallurgical silicon, and oil well cementing.

The washed silica sand market has thousands of companies which thrive in their domestic market. A few of the major players are, Sibelco NV (Belgium), U.S. Silica Holdings, Inc. (US), VRX Silica Limited (Australia), Australian Silica Quartz Group Ltd (Australia), and Adwan Chemical Industries Company (Saudi Arabia), among others. These players have adopted various growth strategies, such as merger & acquisitions, and agreements, to increase their market shares and enhance their product portfolios.

To know about the assumptions considered for the study download the pdf brochure

Merger & acquisition accounted for the largest share of all the strategic developments that took place in the washed silica sand market between 2017 and 2020. Key players such as U.S. Silica Holdings, Inc., and VRX Silica Limited adopted these strategies to enhance their business, market presence, and meet consumer demand.

SCR- Sibelco NV is a global material solutions company. It provides specialty industrial minerals, particularly silica, clays, feldspathic sand, and olivine. The company operates different business segments, namely, Covia, Build Environment; Disposal Group Lime, Glass Solutions; Coating, Polymer & Chemical Solutions; and Water & Environment Solutions. Covia operates with 50 million tons of active production capacity. The company produces the crystalline forms of silica – quartz and cristobalite – as both sands and flours. For industrial use, pure deposits of silica capable of yielding products of at least 98% SiO2 are required. The company has three major silica sand production facilities worldwide. It has 114 production sites that are operating in 31 countries worldwide.

U.S. Silica Holdings, Inc. engages in the provision of commercial silica products. It operates through the Oil & Gas Proppants and Industrial & Specialty Products segments. The Oil & Gas Proppants segment focuses in delivering fracturing sand, which is pumped down oil and natural gas wells to prop open rock fissures and increase the flow rate of natural gas and oil from the wells. The company operates in the US and Canada. It operates 23 production facilities in the US. It controls 489 million tons of reserves of commercial silica, which can be processed to make 197 million tons of finished products.

Request for Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=23955586